It’s thus typical for management personnel to set expectations and benchmarks for both costs and output, while the manufacturing activity is still in its planning stage before the production process even starts. Efficiency variance is the difference between the theoretical amount of inputs required to produce a unit of output and the actual number of inputs used to produce the unit of output. The expected inputs to produce the unit of output are based on models or past experiences. The difference between expected required input and the actual required input can be attributed to inefficiencies in labor or use of resources, or they may be due to errors in the assumptions used to set input expectations. An unfavorable variance means that labor efficiency has worsened, and a favorable variance means that labor efficiency has increased. Before getting started, we wanted to offer an easy way to understand the concept of direct labor efficiency variance with this useful online calculator.

Create a Free Account and Ask Any Financial Question

A positive value of direct labor efficiency variance is obtained when the standard direct labor hours allowed exceeds the actual direct labor hours used. A negative value of direct labor efficiency variance means that excess direct labor hours have been used in production, implying that the labor-force has under-performed. The combination of the unfavorable direct labor efficiency variance of $4,000 + the unfavorable direct labor rate variance of $5,520 is the total unfavorable direct labor variance of $9,520. The direct labor efficiency variance is one of the main standard costing variances, and results from the difference between the standard quantity and the actual quantity of labor used by a business during production. Additionally the variance is sometimes referred to as the direct labor usage variance or the direct labor quantity variance. It is necessary to analyze direct labor efficiency variance in the context of relevant factors, for example, direct labor rate variance and direct material price variance.

How confident are you in your long term financial plan?

At first glance, the responsibility of any unfavorable direct labor efficiency variance lies with the production supervisors and/or foremen because they are generally the persons in charge of using direct labor force. However, it may also occur due to substandard or low quality direct materials which require more time to handle and process. If direct materials is the cause of adverse variance, then purchase manager should bear the responsibility for his negligence in acquiring the right materials for his factory. Based on the standard cost, company spends 5 hours per unit of production. However, they spend 5.71 hours per unit (200,000 hours /35,000 units) on the actual production. Due to the unexpected increase in actual cost, the company’s profit will decrease.

Direct Labor Time Variance

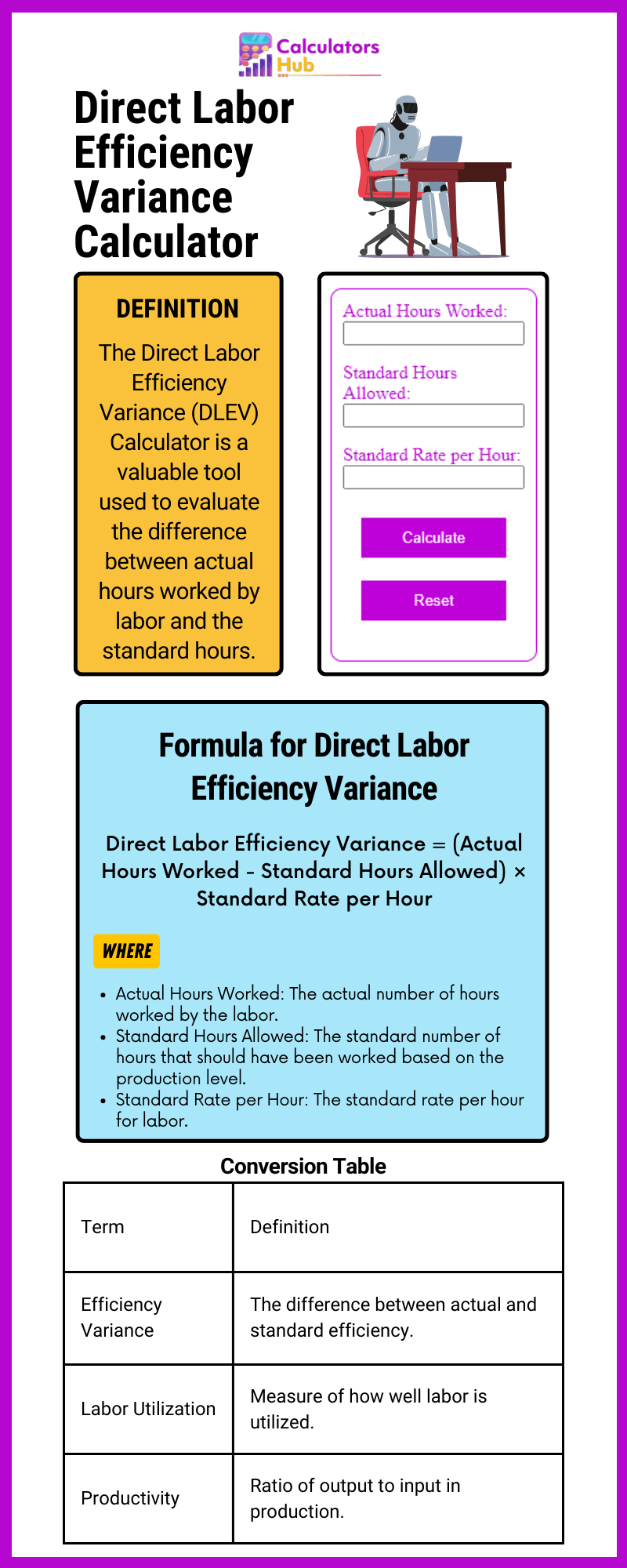

Labor efficiency variance happens when the price per direct labor remains the same but the time spends to produce one unit different from standard costing. Management makes the wrong estimate of the time spent in production or the actual time increase due to various reasons. When the actual time spends different from the estimation, it will lead to a difference of the actual cost and the standard cost. It can be both favorable (actual cost less than the estimate) or unfavorable, the actual is higher than estimate. More specifically, the formula looks at the direct labor hours invested into an outcome (such as the number of units produced) and relates them to the projected labor hours. In simpler terms, the variance tells you exactly how many hours you invested as compared to expectations.

Ask a Financial Professional Any Question

Excessive inventories, particularly those that are still in process, are considered evil as they generally cause additional storage cost, high defect rates and spoil workers’ efficiency. Due to these reasons, managers need to be cautious in using this variance, particularly when the workers’ team is fixed in short run. In such situations, a better idea may be to dispense with direct labor efficiency variance – at least for the sake of workers’ motivation at factory floor.

Ask Any Financial Question

- After getting multiple quotes, you have determined that the standard cost of the job will be 20 hours of labor at $60 per hour.

- Based on the time standard of 1.5 hours of labor per body, we expected labor hours to be 2,430 (1,620 bodies x 1.5 hours).

- This is a favorable outcome because the actual rate of pay was less than the standard rate of pay.

- The first option is not in line with just in time (JIT) principle which focuses on minimizing all types of inventories.

It is quite possible that unfavorable direct labor efficiency variance is simply the result of, for example, low quality material being procured or low skilled workers being hired. Labor efficiency variance is the difference between the time we plan and the actual time spent in production. It is the difference between the actual hours spent and the budgeted hour that the company expects to take to produce a certain level of output. The actual time can be shorter or longer due to various reasons, so it will create a favorable and unfavorable variance. An unfavorable labor efficiency variance signifies that more labor hours were expended than the predetermined standard for the production achieved. It indicates decreased efficiency, where the actual hours surpass the anticipated ones, potentially leading to higher labor costs and inefficiencies within the production process.

Like direct labor rate variance, this variance may be favorable or unfavorable. If workers manufacture a certain number of units in an amount of time that is less than the amount of time allowed by standards for that number of units, the variance is known as favorable direct labor efficiency variance. On the other hand, if workers take an amount of time that is more than the amount of time allowed by standards, the variance is known as unfavorable direct labor efficiency variance. The labor efficiency variance formula is referenced under several names. To be accurate, the formula is used to measure direct labor rate variance. Direct labor variance is a means to mathematically compare expected labor costs to actual labor costs.

DLYV can be affected by several factors, such as labor rate or wage changes, variations in employee skill levels, differences in the number of hours worked, and changes in working conditions. Standard costing plays a very important role in controlling labor costs while maximizing the labor department’s efficiency. In other words, it is the difference between how many hours should have been worked and how many hours were worked, valued at the standard rate per hour.

Continued learning and more-selective hiring are invaluable tools to this end. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

In this case, the actual hours worked per box are \(0.20\), the standard hours per box are \(0.10\), and the standard rate per hour is \(\$8.00\). This is an unfavorable outcome because the actual hours worked were more than the standard hours expected per box. As a result of this unfavorable outcome information, the company may consider retraining its workers, changing the production process to be more efficient, or increasing prices to cover labor costs. Let’s assume the standard for direct labor is 3 hours per unit of output and the standard cost for an hour of direct labor is $10.

Understanding these can help you identify potential issues and implement corrective actions. Hence, variance arises due to the difference between actual time worked and the total hours that should have been worked. This variance tells us how efficient the direct labor was in making the actual output that was produced what is form 1095 by the direct labor. During the planning stages, the management staff might have projected that it will take 50 labor hours to produce one unit of a specific product. However, after the first round of products is completed, records indicate that 65 labor hours were used, to complete the item in question.